The Shift in Underwriting Standards

If your commercial property insurer has recently asked for a thermographic inspection report, you are not alone. Across South Africa and internationally, insurance underwriters are tightening their documentation requirements for electrical risk — and thermographic surveys are at the centre of that shift.

The reasons are straightforward: electrical failures remain one of the leading causes of commercial property damage and business interruption claims, and insurers have the loss data to prove it. Fire was identified as the number one financially damaging risk for South African businesses in 2025, with most incidents linked directly to electrical faults, aged wiring, and overloaded systems.

What Changed in the Standards

The 2023 update to NFPA 70B — the Recommended Practice for Electrical Equipment Maintenance — made annual infrared inspections mandatory for energised electrical equipment under condition-based maintenance programmes. While NFPA 70B is an American standard, South African insurers and underwriters reference it directly, and its adoption into local underwriting requirements has accelerated significantly since 2024.

Locally, SANS 10142-1 specifies that electrical installations be maintained in a safe condition. Insurers interpret this as requiring documented preventative maintenance — and thermographic inspection is the most accepted form of that documentation for electrical systems.

Insurers who commonly request thermographic reports in South Africa

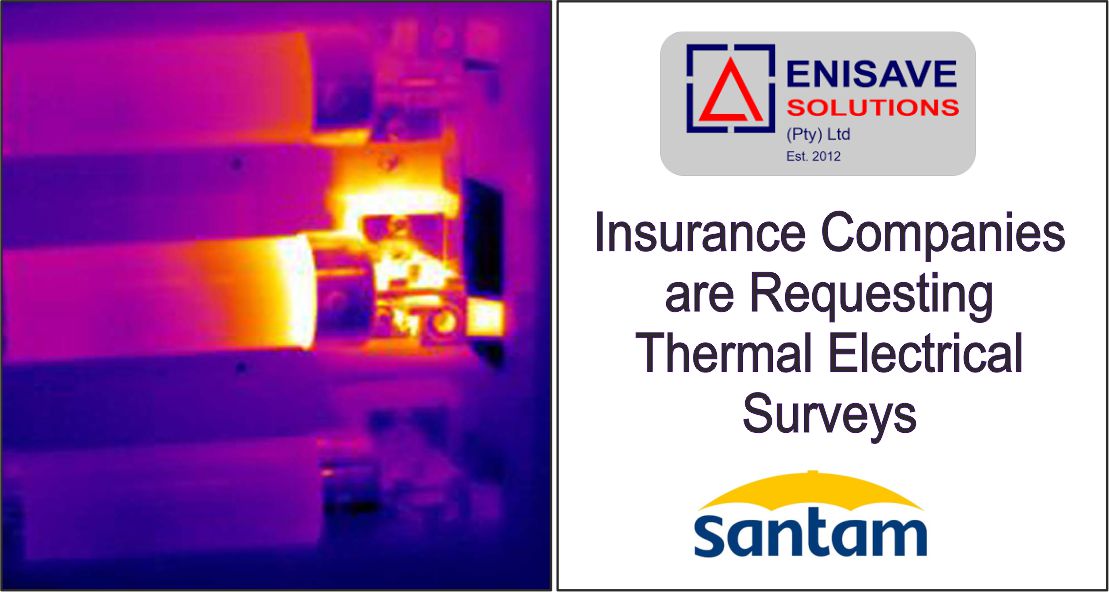

Santam, Old Mutual Insure, Hollard, Bryte Insurance, and Mutual & Federal all reference thermographic inspection compliance in their commercial and industrial underwriting requirements. The specific requirements vary by policy type, property size, and risk profile — but the direction of travel is consistent across all major carriers.

Why Electrical Risk Is a Priority for Underwriters

Several factors are driving increased insurer scrutiny of electrical risk specifically:

- Ageing infrastructure — many South African commercial and industrial facilities operate electrical systems that are 20 to 40 years old, well beyond their design life. The failure probability of aged switchgear, cable insulation, and terminations increases significantly with time.

- Load growth without infrastructure upgrades — facilities have added equipment, expanded operations, and increased electrical loads without proportional upgrades to the distribution infrastructure. Overloaded circuits and undersized conductors are common findings in older installations.

- Business interruption exposure — modern facilities depend on continuous power. Even a short outage triggered by an electrical fault can cause losses far exceeding the physical damage cost. Insurers price this exposure into their underwriting requirements.

- Claims data — insurers have sufficient loss history to demonstrate that facilities with documented thermographic maintenance programmes have materially lower fire and equipment failure claim frequencies than those without.

What the Report Needs to Contain

Not all thermographic reports satisfy underwriter requirements. A report that will be accepted for insurance compliance purposes needs to include:

- Confirmation that the survey was conducted at or above 40% of rated load

- Visible light and thermal image pairs for each identified finding

- Temperature measurements and ΔT calculations versus reference

- Severity classification for each finding (P1 Critical through P4 Low, or equivalent)

- Specific recommended corrective actions per finding

- Thermographer qualifications and certification details

- Survey date, site details, and equipment coverage scope

Reports produced by unqualified or under-equipped surveyors — or surveys conducted at low load — are increasingly being rejected by underwriters, requiring repeat surveys at the policyholder's cost.

What Santam's Preferred Supplier Status Means

Enisave Solutions is a Santam Insurance Preferred Supplier for thermographic inspection services. This designation means our reports are accepted directly by Santam underwriters without additional verification. For clients insured with Santam, an Enisave survey report satisfies the thermographic inspection requirement at renewal.

For clients insured with other carriers, our reports are structured to meet the documentation requirements of all major South African insurers and are accompanied by a compliance summary that facilitates direct submission.

What to Do If Your Insurer Has Asked for a Report

If you have received a request from your insurer or broker for a thermographic inspection report, the process is straightforward:

- Contact Enisave Solutions to schedule a survey — we will advise on scope and timing

- Ensure the survey is conducted under normal operating load conditions

- Receive the completed report, typically within 5 working days of the survey

- Submit the report to your insurer or broker with the compliance summary

- Address Priority 1 (Critical) findings immediately — insurers may require evidence of corrective action for serious findings

Need a Report for Your Insurer?

We produce insurance-grade thermographic reports accepted by Santam and all major South African insurers.

Schedule a Survey